W-2 and Last Pay Stub: What’s the Difference?

As tax season approaches, many employees wonder why their W-2 and last pay stub don’t always match—especially when it comes to gross income. Understanding how gross income on a W-2 differs from what’s shown on a pay stub can help clarify your taxable wages and deductions.

This article will explore why a W-2 and pay stub might show different amounts and answer common questions like, “Why doesn’t my W-2 match my last pay stub?” and “Why does my W-2 not match my salary?” Use this resource as a way to answer your employees’ questions and make tax season a smoother experience.

Is a W-2 the Same as a Pay Stub?

No, a W-2 and a pay stub are different. A W-2 form, also known as a Wage and Tax Statement, is a required document that an employer must send to employees each year. Once an employee elects their preferred withholdings like healthcare and 401(k) contributions, the employer must send a receipt of that information to the Internal Revenue Service (IRS) for reporting purposes. Think of your employees’ W-2 as a net earnings pay stub.

A pay stub outlines the details of an employee’s gross wages for each pay period. Employers are not required to send pay stubs to employees. However, the Fair Labor Standards Act (FLSA) requires employers to track employees’ work hours.

A pay stub is typically attached to an employee’s physical paycheck. Certain payroll providers also offer paperless payroll, allowing employees to access pay stubs online.

The end of year pay stub reflects gross wages, including non-taxable income and deductions. Therefore, W-2 wages are typically lower than gross wages because of pre-tax deductions like healthcare or retirement contributions.

Does Your Workforce Have W-2 Questions?

Why is My W-2 Different from My Last Pay Stub?

Employees often ask, “Why is my W-2 different from my last pay stub?” The reason is simple: your pay stub earnings include gross income, while your W-2 reflects taxable income. Additionally, pre-tax deductions lower the taxable amount reported on the W-2, which is why an employee’s final pay stub and W-2 differ.

Common Reasons for W-2 and Pay Stub Differences

- Pre-Tax Deductions: Contributions to retirement plans, health insurance, flexible spending accounts, and other benefits. These deductions are reflected in your W-2 but may not show on your year-end pay stub.

- Non-Taxable Income: Items like mileage reimbursements or allowances aren’t included in your W-2, making your last pay stub appear higher than your W-2.

- Retirement Plan Contributions: Contributions to retirement plans like 401(k)s reduce the income reported in Box 1 of your W-2. For example, if your gross wages are $50,000, but you contributed $5,000 to a 401(k), your taxable wages in Box 1 of your W-2 will be $45,000.

| Pay Stubs | W-2s |

|---|---|

| Gross Dollar Amount of Salary | Taxable Wages Reported |

| Before Taxes | After Pre-Tax Deductions Get Taken Out (Health insurance, Life Insurance, 401(k), Disability insurance) |

Unless you opt out of pre-tax deductions, your salary amount will almost always be higher than the wages reported on your W-2. To clarify which pre-tax deductions you are opted in to, check Box 1 of your W-2. If you are confused about your Box 1 deductions, our blog Pre-Tax and Post-Tax Deductions: What’s The Difference can help clarify details related to these withholdings.

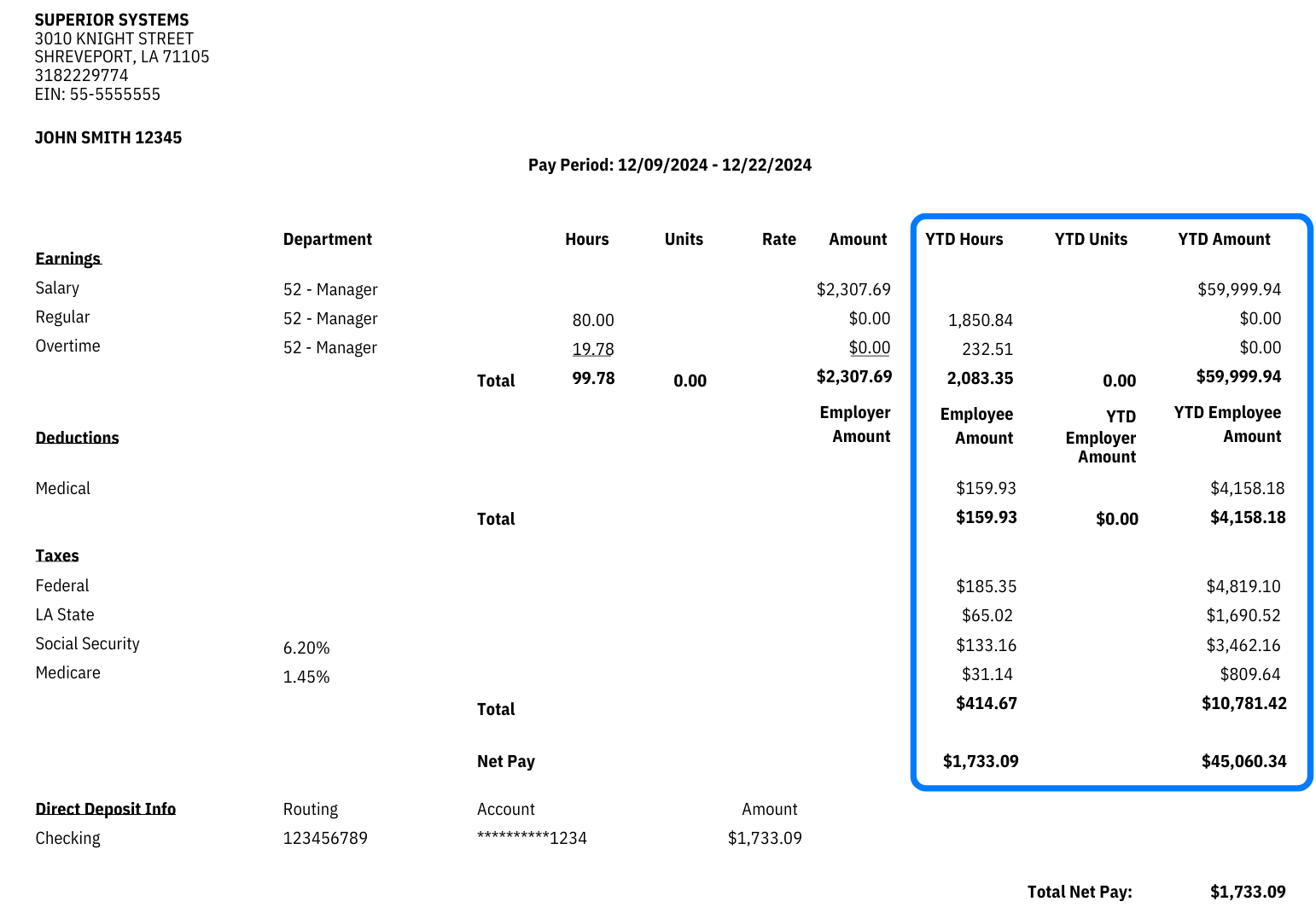

Reasons Why the Gross Amount on Your End-of-Year Pay Stub May be Different Than the Amount on Your W-2

APS receives many questions during tax season, and the one that comes up most often is, “Why doesn’t my W-2 match my pay stub?” or “Why doesn’t my W-2 match my salary?” It is typical for gross taxable wages on an employee’s final pay stub of the year to differ from the amount shown on their Form W-2.

Let’s look at some examples of the common reasons why W-2 and paystub amounts are different:

1. Year-End Pay Stubs Include Non-Taxable Income Items

Examples of non-taxable income items include reimbursements for mileage or other non-taxable expenses. These non-taxable items are paid back during payroll runs. As a result, the gross wages on an employee’s pay stub often differ from Boxes 1, 3, 5, and 16 wages on the W-2 because these non-taxable items will lower gross taxable wages.

Example

Mary’s gross wages are $30,000, but she received $2,000 towards a non-taxed car allowance over the year. Mary’s taxable W-2 wages will be $28,000.

($30,000 – $2,000 = $28,000)

2. Company-Sponsored Retirement Plan Participation

Company-sponsored retirement plans like 401(k)s only reduce taxable federal and state wages. They are reported in Boxes 1 and 16, respectively. If you contribute to a retirement plan, the compensation on your end-of-year pay stub vs. your W-2 will differ.

Example

Sally’s gross wages are $30,000, but she contributed $3,000 towards her 401(k) retirement over the year. Sally’s federal and state W-2 wages will be $27,000.

($30,000 – $3,000 = $27,000)

3. Company Health Insurance is a Pre-Tax Deduction

Company health insurance is the most common reason your last pay stub does not match your W-2. If your company offers pre-tax health insurance and you have participated, then the taxable wages in Boxes 1, 3, 5, and 16 will be lower than the pre-tax health insurance deduction amount. Pre-tax deductions will lower the gross wages by the annual amount of the deduction.

Example

John’s gross wages are $30,000, but he contributed $2,000 to a pre-tax health insurance deduction over the year. John’s taxable W-2 wages will be $28,000.

($30,000 – $2,000 = $28,000)

Why Doesn’t My W-2 Match My Salary?

Another common question is, “Why does my W-2 not match my salary?” Your salary is the total amount earned before any deductions. However, your W-2 reflects taxable wages, which are reduced by pre-tax deductions such as 401(k) or health insurance.

Therefore, the W-2 amount is usually lower. This is why your W-2 doesn’t match your last pay stub or salary.

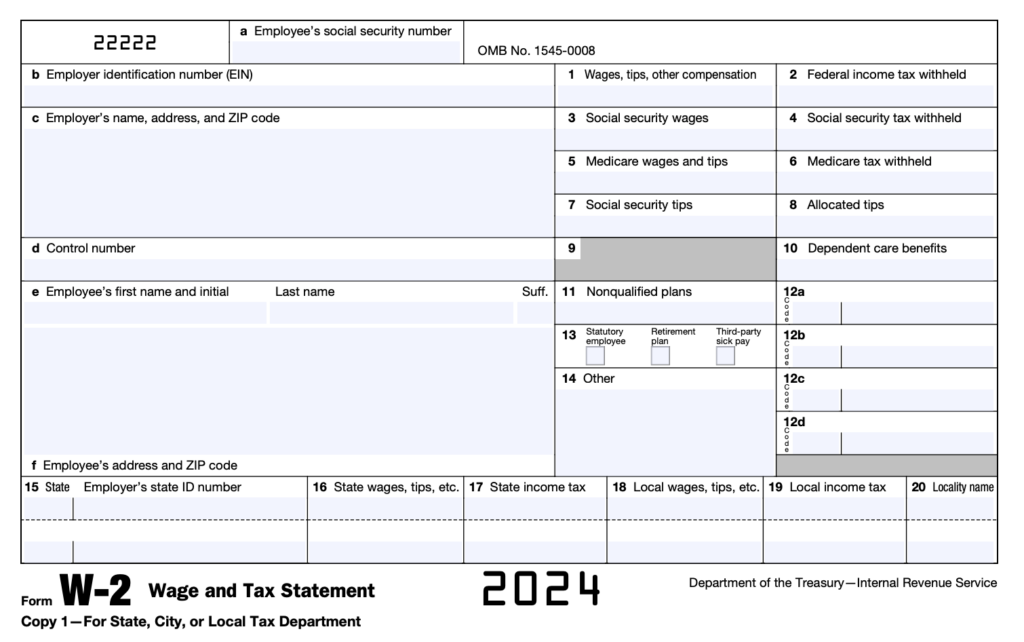

What are the Boxes on a W-2?

Now that you better understand the W-2 vs. last pay stub, it’s time to discuss the boxes on Form W-2.

Box 1: Wages, Tips, and Other Compensation

Box 1 shows the amount of gross taxable wages an employer paid. These wages include tips, bonuses, commissions, and salaries. This part of Form W-2 doesn’t include amounts given to retirement plans or other payroll deductions. Because it subtracts other deductions, it’s often less than the amounts shown in Boxes 2 and 3. Therefore, it may be lower than the amount on a final pay stub.

Box 2 – Federal Income Tax Withheld

Box 2 shows the Federal income tax withheld from your pay during the previous calendar year. The W-4 you fill out each year determines this tax withholding rate. If your employees find their tax number too high or low, encourage them to adjust their Form W-4 since this information directly affects Box 2 of the W-2.

Box 3 – Social Security Wages

Box 3 includes the number of earnings your employer paid you – not including tips – subject to Social Security tax. The number in this box doesn’t consider pretax deduction items that reduce overall taxable income, which means Box 3 could be higher than the amount shown in Box 1.

However, if you or your employee are high-income earners, this box could be less than the total amount in Box 1. That’s because there is a maximum amount of wages Social Security can tax high-income earners. The maximum Social Security tax for high-income earners in 2024 is $168,600.

Box 4 – Social Security Tax Withheld

This amount represents the total social security taxes withheld from your wages. Box 4 gets calculated as 6.2 percent of the Social Security wages in Box 3. You shouldn’t have more Social Security withholding than the maximum wage base x 6.2%.

Box 5 – Medicare Wages and Tips

Medicare wages and tips are the total amount of earnings you make that are subject to Medicare tax. These taxes don’t usually subtract pre-tax deductions and include taxable benefits like bonuses and vacation. There also isn’t a cap on Medicare taxes, which means the number in Box 5 can be significantly larger than what’s shown in Box 1 or Box 3.

Box 6 – Medicare Tax Withheld

Medicare tax withheld represents the amount Medicare deducted from your wages for taxes. Both Social Security and Medicare taxes come from a flat rate. The rate is usually 1.45% percent of the total Medicare wages in Box 5.

An easy formula for this is Box 6 = Box 5 x 1.45%. However, employees who earn more than $200,000 (single) or $250,000 (married filing jointly) are also subject to an additional 0.9 percent Medicare tax.

Box 7 – Social Security Tips

This box represents tips subject to Social Security Tax. If this box is blank, you didn’t report any tips earned to your employer. However, unreported tips are still taxable. The amount in this box and Box 3 should total the amount in Box 1.

Box 8 – Allocated Tips

This box shows the tip income your employer allocated to you. W-2 boxes 1, 3, 5, or 7 don’t include this amount. To learn more about tip income, click here.

Box 9 – Not in Use

This box was for the 16-digit code issued to employers who participated in the IRS Verification Initiative but is no longer in use. It applied only to electronically filed returns and was intended to combat tax identity theft and refund fraud.

Box 10 – Dependent Care Benefits

Box 10 lists the total amount paid into your dependent care flexible spending account for the year. Any amount over $5,000 is included in Box 1 as well.

Box 11 – Nonqualified Plans

This box shows the total amount distributed to you from your employer’s nonqualified deferred compensation plan. This amount is taxable and is not to be confused with the amounts listed in Box 12. Box 11 is distributed to you, while Box 12 gets distributed by you.

Box 12 – Compensation and Benefits

This box indicates compensation or benefits by code. Not all Box 12 codes are taxable. Here is more information on each code:

- A — Uncollected Social Security or RRTA tax on tips

- B — Uncollected Medicare tax on tips (but not Additional Medicare tax)

- C — Taxable cost of group-term life insurance over $50,000

- D — Elective deferrals under a section 401(k) cash or deferred arrangement plan (including a SIMPLE 401(k) arrangement)

- E — Elective deferrals under a section 403(b) salary reduction agreement

- F — Elective deferrals under a section 408(k)(6) salary reduction SEP

- G — Elective deferrals and employer contributions (including nonelective deferrals) to a section 457(b) deferred compensation plan

- H — Elective deferrals to a section 501(c)(18)(D) tax-exempt organization plan

- J — Nontaxable sick pay

- K — 20% excise tax on excess golden parachute payments

- L — Substantiated employee business expense reimbursements

- M — Uncollected social security or RRTA tax on taxable cost of group-term life insurance over $50,000 (former employees only)

- N — Uncollected Medicare tax on taxable cost of group-term life insurance over $50,000 (but not Additional Medicare Tax) (former employees only)

- P — Excludable moving expense reimbursements paid directly to members of the Armed Forces

- Q — Nontaxable combat pay

- R — Employer contributions to an Archer MSA

- S — Employee salary reduction contributions under a section 408(p) SIMPLE plan

- T — Adoption benefits

- V — Income from exercise of nonstatutory stock option(s)

- W — Employer contributions (including employee contributions through a cafeteria plan) to an employee’s health savings account (HSA)

- Y — Deferrals under a section 409A nonqualified deferred compensation plan

- Z — Income under a nonqualified deferred compensation plan that fails to satisfy section 409A

- AA — Designated Roth contributions under a section 401(k) plan

- BB — Designated Roth contributions under a section 403(b) plan

- DD — Cost of employer-sponsored health coverage

- EE — Designated Roth contributions under a governmental section 457(b) plan

- FF — Permitted benefits under a qualified small employer health reimbursement arrangement

- GG — Income from qualified equity grants under section 83(I)

- HH — Aggregate deferrals under section 83(i) elections as of the close of the calendar year

- II — Medicaid waiver payments excluded from gross income under Notice 2014-7

Box 13 – Retirement Plan

This box is checked when an employee actively participates in a retirement plan. For more information, see the Box 13 Retirement Plan Checkbox Decision Chart on the IRS W-2 form.

Box 14 – Other

This box reports miscellaneous information:

- State disability insurance taxes withheld

- Union dues

- Uniform payments

- Deducted health insurance premiums

- Nontaxable income

- Educational assistance payments

- A member of the clergy’s parsonage allowance and utilities

- Charitable contributions made through payroll deduction

Box 15- Employer’s State ID Number

Box 15 is where you list your employer’s state and tax identification number. If you work in a state that doesn’t require W-4 reporting, Box 15, 16, and 17 will be blank. However, more than one box will get filled if you have multiple withholdings in various states. Here’s a list of states that don’t require this reporting:

- Alaska

- Florida

- Nevada

- New Hampshire

- South Dakota

- Tennessee

- Texas

- Washington

- Wyoming

Box 16 – State Wages, Tips, Etc.

Box 16 represents the number of your wages subject to state tax. The amount might differ from the amount shown in Box 1. This box will remain blank if you don’t live in a state with income taxes.

Box 17 – State Income Tax

If you reported wages in Box 16, then Box 17 will show the amount of state taxes withheld from you and your employee’s income. If you live in a state with a flat state tax, it’s good to double-check withholdings by multiplying the amount in Box 16 by that state’s tax rate.

State income taxes can impact final pay stubs and W-2s. Employees should be mindful of varying state taxes and how moving from one state to another can affect their year-end documents.

Here is a list of states with flax tax rates. This list is subject to change.

- Arizona – 2.50%

- Colorado – 4.40%

- Georgia – 5.49%

- Idaho – 5.80%

- Illinois – 4.95%

- Indiana – 3.05%

- Iowa – 4.00%

- Kentucky – 4.25%

- Michigan – (4.70% on all income after the first $10,000)

- Mississippi – (3.00% tax on interest and dividend income only; the state is phasing it out and has scheduled this tax to cease after December 31, 2026)

- North Carolina – 4.50%

- Pennsylvania – 3.07%

- Utah – 4.65%

Box 18 – Local Wages, Tips Etc.

If you or your employees live in an area subject to local, city, or other state income taxes, those wages get reported here. When employees have wages subject to withholding in more than two states or localities, you need to provide them with an additional W-2 form.

Box 19 – Local Income Tax

Any taxes withheld on the wages in Box 18 get reported in Box 19.

Box 20 – Locality Name

Box 20 is where you put the name of the local area, city, or other state tax reported in Box 19.

Download the Year-End Payroll Guide

Want to take it with you? Download our convenient guide to make your year-end payroll processing easier.

Can I Use My Last Pay Stub as a W-2 for Taxes?

While your last pay stub can provide an estimate of your taxable income, the IRS recommends using the official W-2 for tax filing. The W-2 includes specific tax information and deductions that may not be fully reflected on your pay stub. Tools like a pay stub to W-2 converter can help estimate, but the IRS recommends using official tax documents for filing.

Frequently Asked Questions About W-2s and Pay Stubs

Why doesn’t my W-2 match my last pay stub?

Employees may ask, “Why does my W-2 not match my last pay stub?” or “Why is my W-2 different from my last paycheck?” Your W-2 reflects taxable wages after deductions, while your last pay stub includes all gross earnings. Pre-tax deductions like healthcare and retirement plan contributions reduce the taxable wages reported on the W-2.

Why does my W-2 not match my salary?

Your salary is the total amount you earned before taxes and deductions, while your W-2 shows the wages you were taxed on. Pre-tax deductions lower the amount on your W-2, which is why it may be less than your salary.

Why is my W-2 less than my salary?

Your salary represents the gross pay before deductions. The W-2 reflects only your taxable wages after accounting for pre-tax deductions, so it will often show a lower amount.

Why is my W-2 higher than my salary?

If your W-2 shows a higher amount than expected, it could be because of taxable income not considered part of your regular salary, such as bonuses or tips. Additionally, if your W-2 includes certain benefits or deferred compensation, the reported amount may be higher than just your base salary.

Is your last pay stub the same as a W-2?

No, your last pay stub shows all earnings for the year, but your W-2 only reports taxable wages. Therefore, your last paycheck of the year may include non-taxable income, making it appear higher than the W-2.

Why is my gross pay different from my W-2?

Your gross pay on a pay stub includes all earnings before deductions, while your W-2 reports only your taxable wages. The difference is usually because of pre-tax contributions like health insurance or 401(k) plans, which lower the taxable wages reported on the W-2.

Is W-2 gross or net income?

Another common question is “Does W-2 show gross or net income?” or “Is wages on W-2 gross or net?” A W-2 shows your gross taxable income or gross taxable wages, which is different from your net income (take-home pay). It reflects the amount before taxes and other deductions like healthcare and retirement contributions.

How APS Can Help

APS helps organizations of all sizes and industries with payroll processing and tax compliance needs. We understand that payroll, W-2 forms, and tax deductions are challenging. That’s why we closely monitor all tax regulation changes to ensure we minimize customer compliance burdens. Here’s how we can help you navigate payroll taxes:

- We automate the management of incomes and deductions during payroll processing to ensure accurate withholdings and paychecks.

- Our secure, centralized database stores and tracks required tax forms for employees for better payroll and tax compliance.

- Our Analytics and Reporting solution provides employee classification reports so that you can maintain compliance.

- Our payroll and tax compliance experts file federal, state, and local tax filings and payments as the reporting agent on your behalf.

- We provide wage garnishment services, including calculating and processing garnishment orders, so you don’t pay unnecessary penalties.

- Our built-in W-2 error-checking algorithm and validation rules allow you to review incomes and deductions before processing payroll to ensure accuracy.

- Our tax compliance department helps you with other tax regulations saving you time and money.

Contact us today to learn more about how APS can make your payroll processing and tax compliance easier.

Clarifying W-2s and Pay Stubs

Employees often want to understand the difference between a W-2 and a pay stub, and they will ask their HR manager for clarification. Remember to tell them that the W-2 reflects taxable wages while the end-of-year pay stub includes gross earnings before deductions.

If they are still unsure, provide them with a resource like this article or our handout for further clarification on how a W-2 and last pay stub relate to each other.

Sources

- About Form W-2

- What is a Pay Stub and What Should it Include?

- Fair Labor Standards Act (FLSA)

- What Are Pre-Tax Deductions?

- What is Taxable and Nontaxable Income?

- Retirement Topics – Contributions

- Tip Recordkeeping and Reporting